Data Center

Access our research through the lens of our charts and tables. View all of our charts (sorted by publishing date) on the left, and click on any chart to read the report in which it appeared.

Select the image you are interested in to load the corresponding report in the content section. This intuitive layout ensures that you can easily find and view reports based on their visual thumbnails.

-

Broadening Leadership Behind the Rally & All Eyes on AAPL

Thu, April 30, 2026 | 7:31PM ET -

Broadening Leadership Behind the Rally & All Eyes on AAPL

Thu, April 30, 2026 | 7:31PM ET -

Broadening Leadership Behind the Rally & All Eyes on AAPL

Thu, April 30, 2026 | 7:31PM ET -

Broadening Leadership Behind the Rally & All Eyes on AAPL

Thu, April 30, 2026 | 7:31PM ET -

Broadening Leadership Behind the Rally & All Eyes on AAPL

Thu, April 30, 2026 | 7:31PM ET -

Broadening Leadership Behind the Rally & All Eyes on AAPL

Thu, April 30, 2026 | 7:31PM ET -

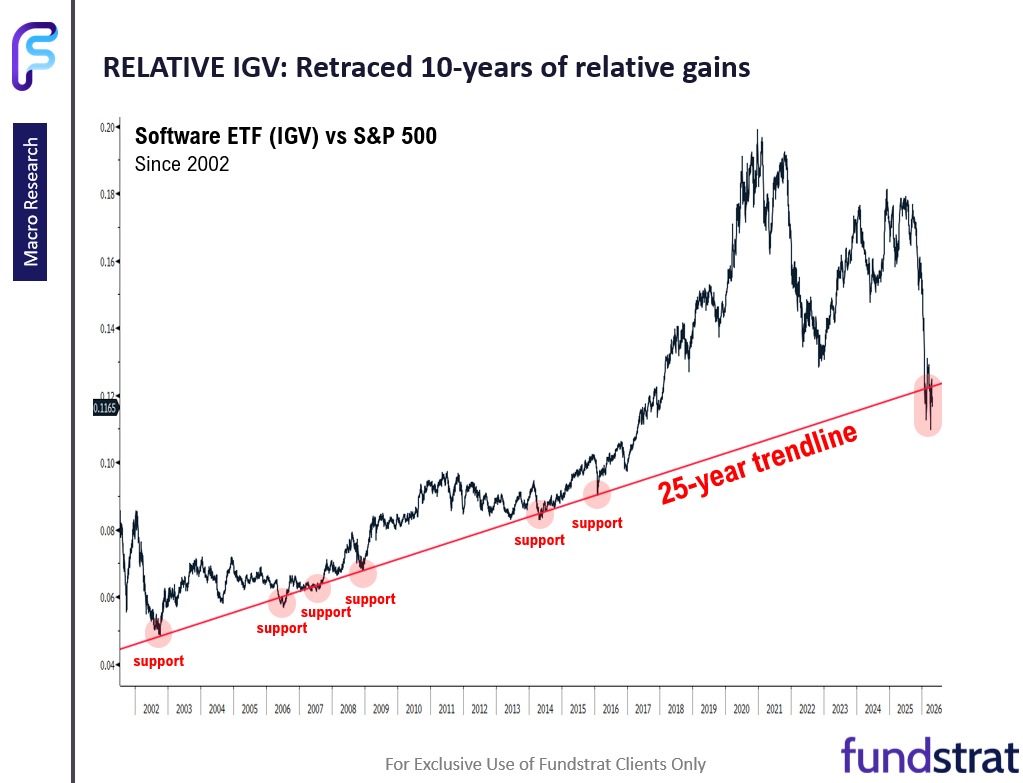

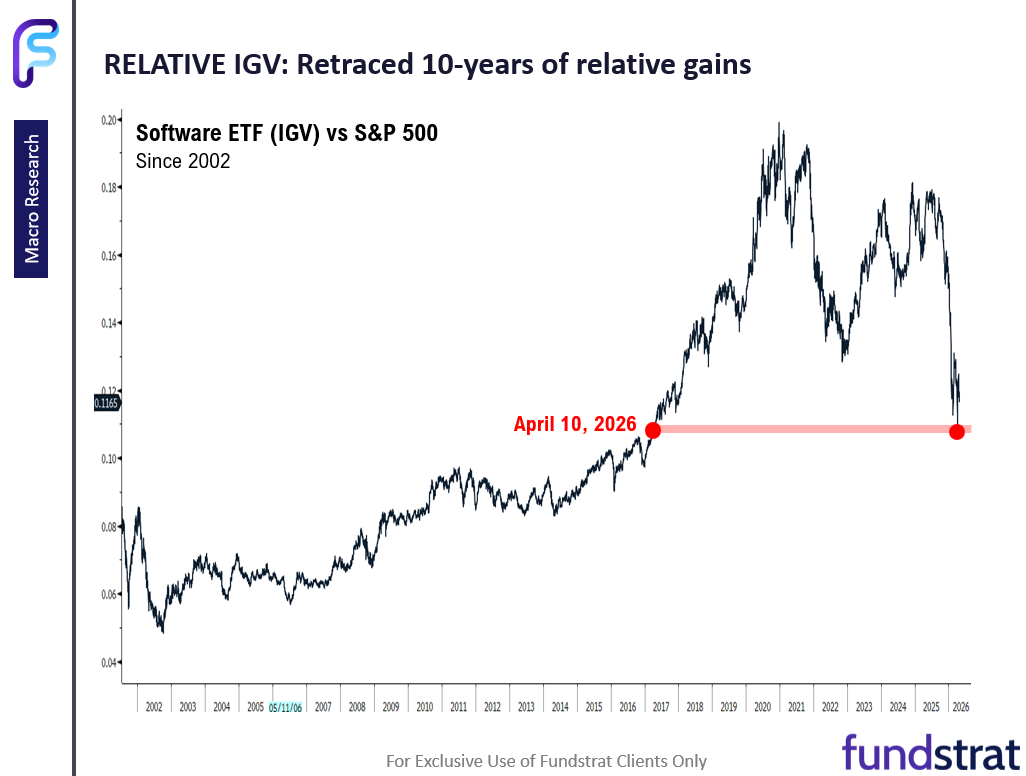

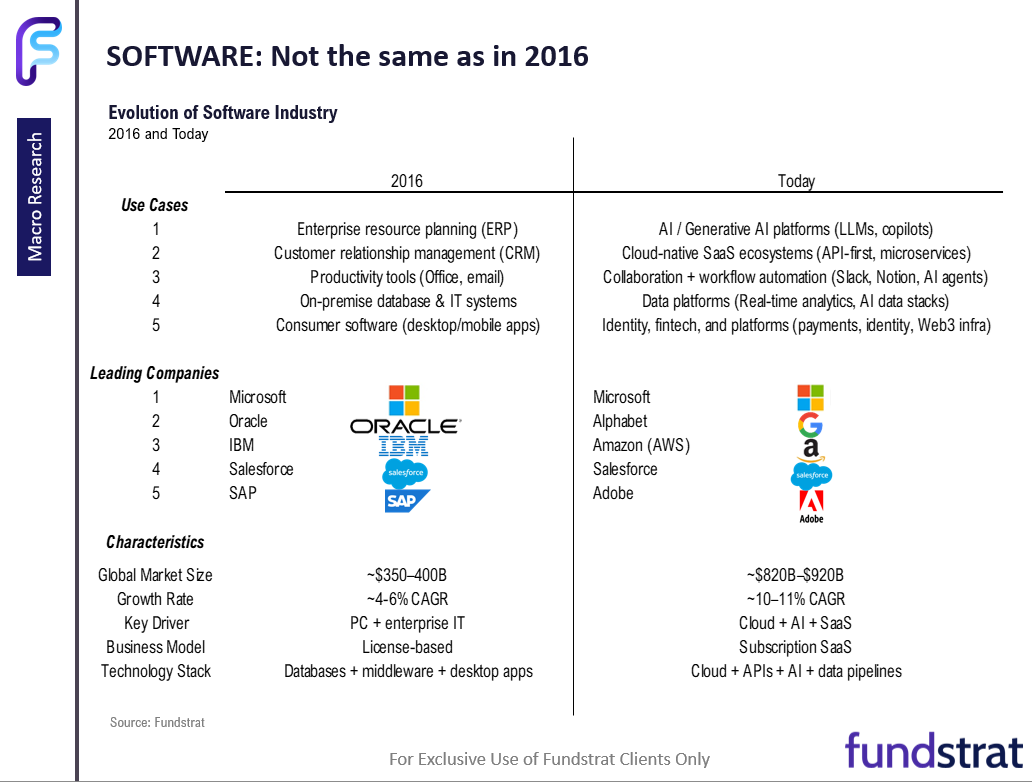

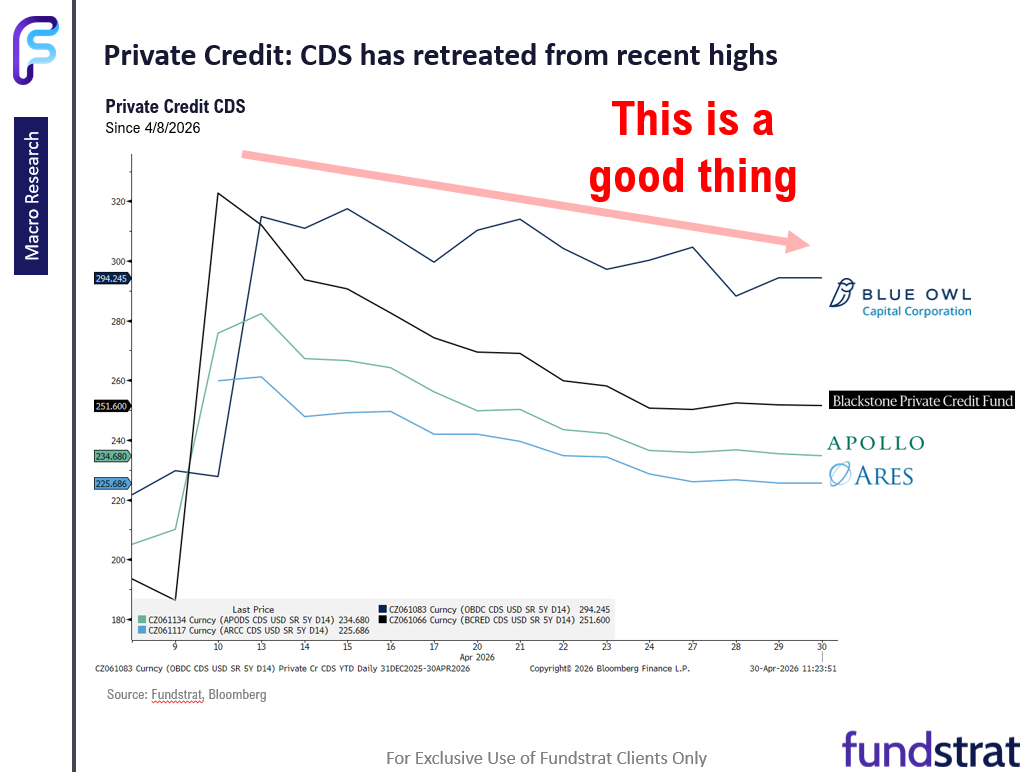

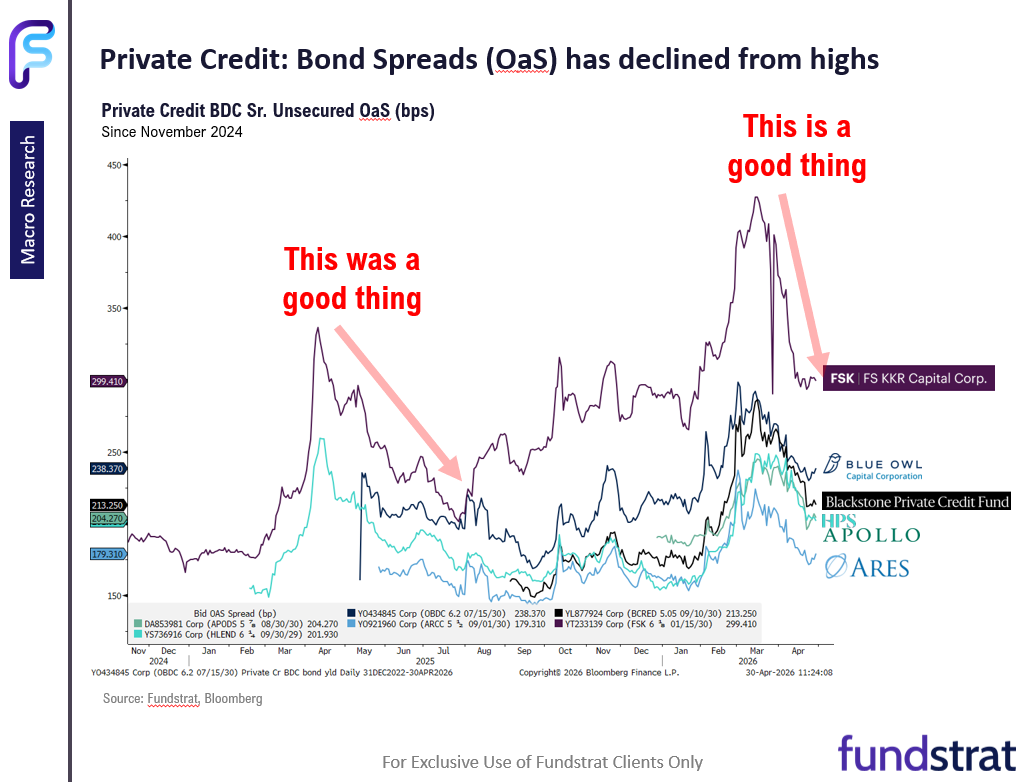

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

Adding Software $IGV to top sector ideas along with $MAGS $IBIT $ETHA. If correct, private credit risks diminishing

Thu, April 30, 2026 | 6:55PM ET -

What Kind of a CEO Will Apple’s John Ternus Be?

Thu, April 30, 2026 | 8:45AM ET -

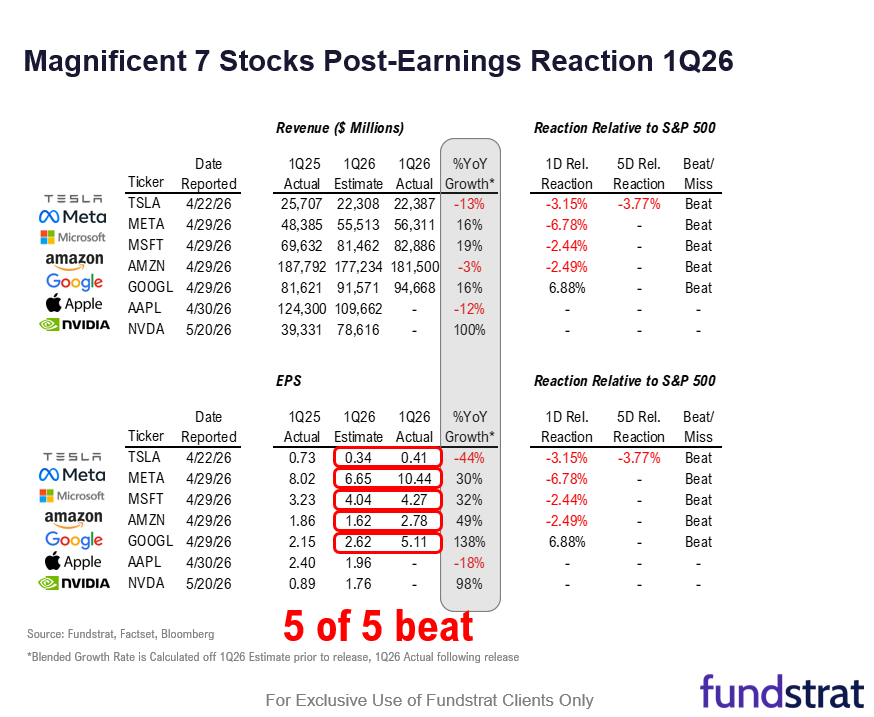

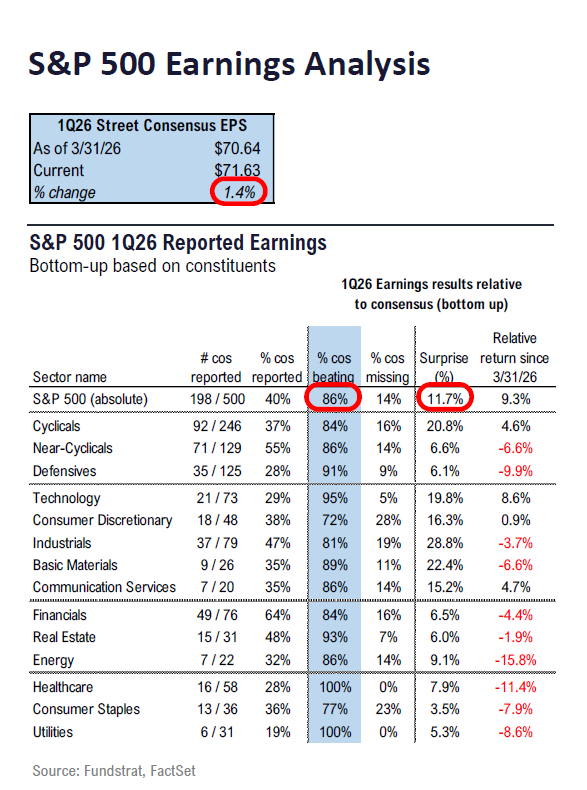

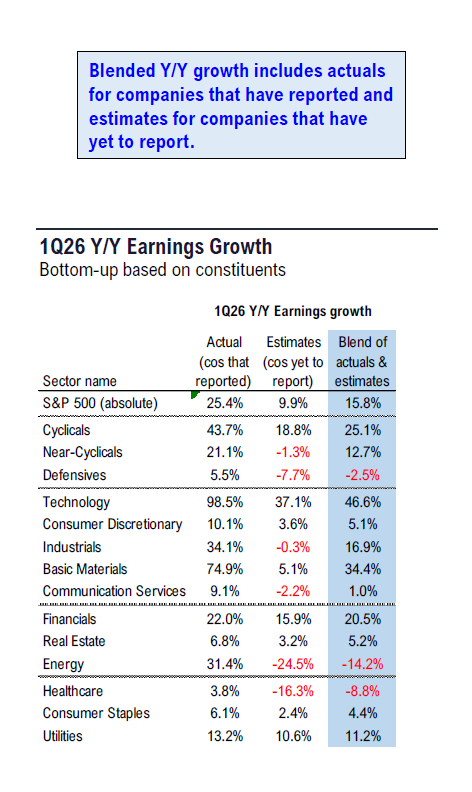

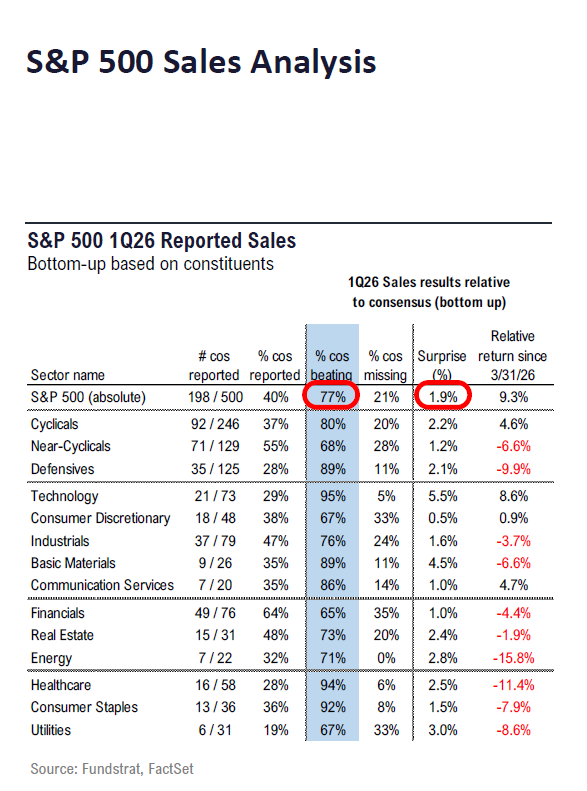

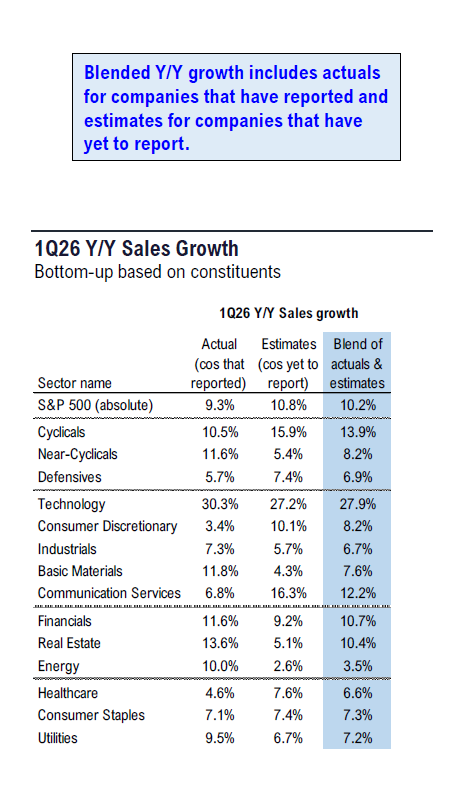

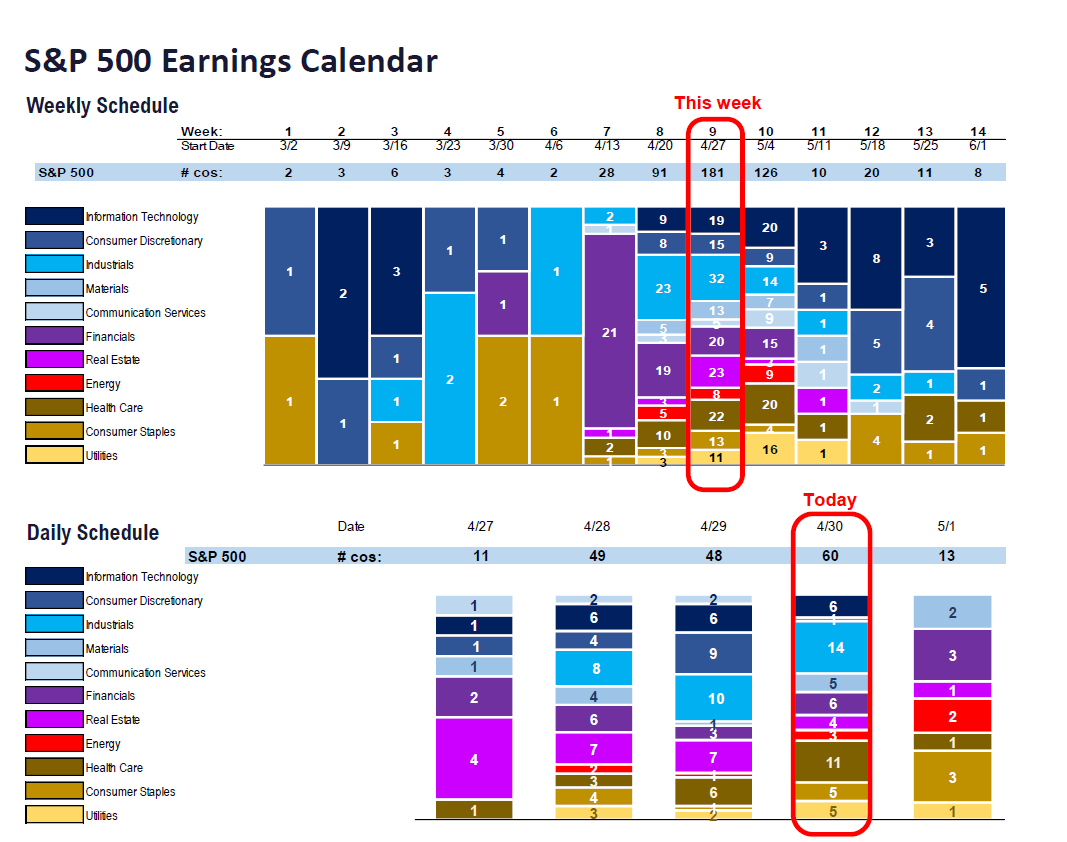

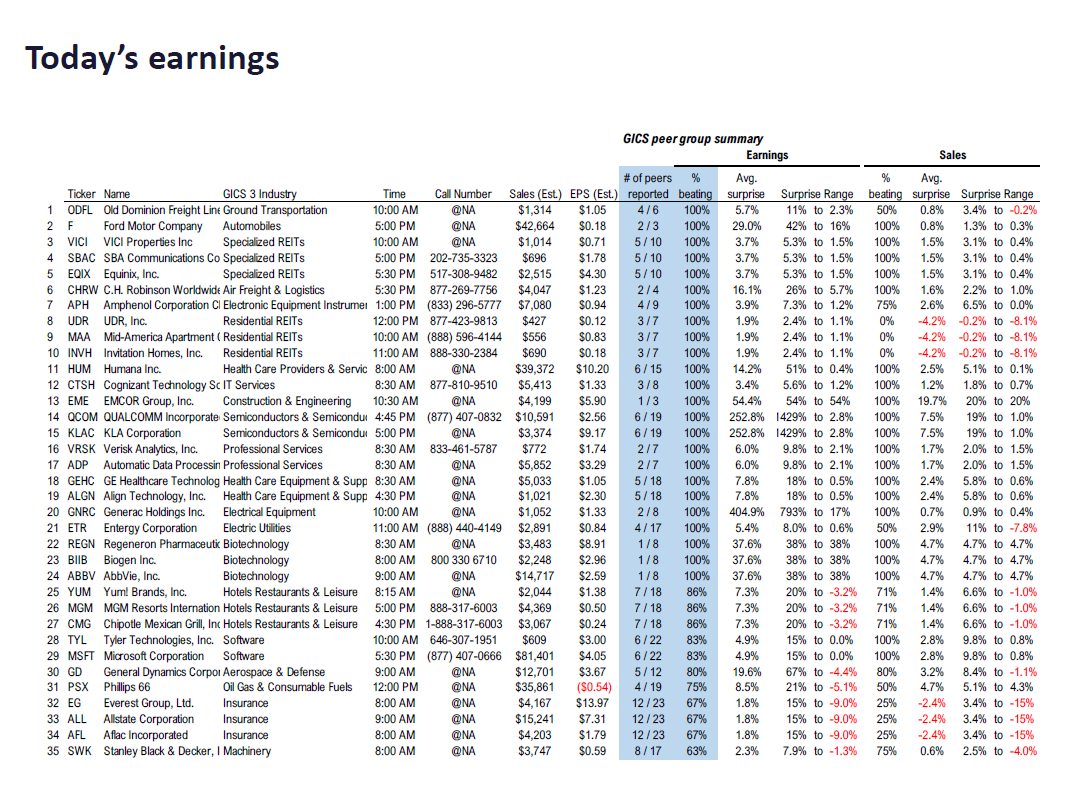

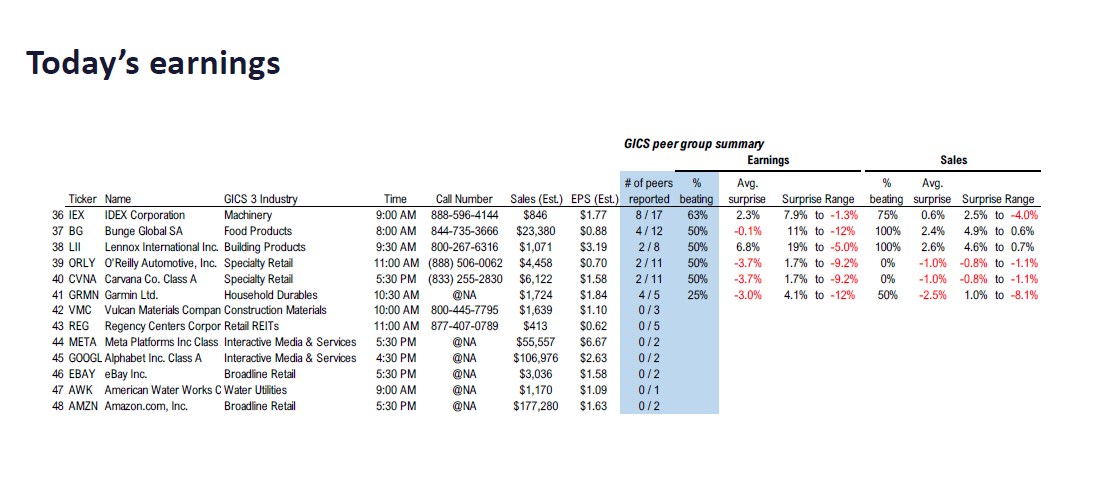

Fundstrat 1Q26 Daily Earnings (EPS) Update – 04/30/2026

Thu, April 30, 2026 | 6:30AM ET -

Fundstrat 1Q26 Daily Earnings (EPS) Update – 04/30/2026

Thu, April 30, 2026 | 6:30AM ET -

Fundstrat 1Q26 Daily Earnings (EPS) Update – 04/30/2026

Thu, April 30, 2026 | 6:30AM ET -

Fundstrat 1Q26 Daily Earnings (EPS) Update – 04/30/2026

Thu, April 30, 2026 | 6:30AM ET -

Fundstrat 1Q26 Daily Earnings (EPS) Update – 04/30/2026

Thu, April 30, 2026 | 6:30AM ET -

Fundstrat 1Q26 Daily Earnings (EPS) Update – 04/30/2026

Thu, April 30, 2026 | 6:30AM ET -

Fundstrat 1Q26 Daily Earnings (EPS) Update – 04/30/2026

Thu, April 30, 2026 | 6:30AM ET

Mark L. Newton, CMT AC

Broadening Leadership Behind the Rally & All Eyes on AAPL

Key Takeaways

- $SPX has cleared 7200 with a near-term target now of 7250-7300; Today's broadening leadership should allow $RSP, $DJIA, and $IWM to follow $SPX and $QQQ to new all-time highs

- All eyes on $AAPL — a constructive technical setup positions the name to participate in the next leg higher, with $RSP en-route to 208 above prior 205 highs.

- AAII Sentiment is a refreshing tell for bulls — bullish respondents barely outpace bearish ones despite the recent rally, with elevated Neutral readings indicating no speculative positioning or complacency to fade.

Near-term US Equity trends remain quite constructive, with ^SPX1.06% having pushed back above 7200 and a near-term target now of 7250-7300 in the days ahead. Today’s broadening of leadership is encouraging technically and gives me confidence that this rally has more gas in the tank — equal-weighted RSP1.43% has reached multi-day highs, and in my view, both RSP1.43% , DJIA1.08% , and IWM2.24% should follow ^SPX1.06% and QQQ0.97% to new all-time highs over the next 3-5 trading days. Sectors like Industrials, Consumer Discretionary, REITS, Consumer Staples, and Healthcare all joined Technology in rising more than 1%, which was seen as much needed after the recent minor breadth deterioration. All eyes are on AAPL0.63% into earnings, where a constructive technical setup positions the name to participate in the next leg higher. Overall, technically speaking, it’s right to lean bullish here and use any further weakness to add exposure — broader participation, healthy sentiment, and no complacency leave more room for this rally to extend.

Apple Inc. (AAPL0.63% ) – All eyes on AAPL — pushing higher and consolidation lately near the resistance trendline argues for a coming breakout

AAPL0.63% looks well-positioned to try to extend and break out after its earnings tonight, given the cluster of consolidation near the resistance trendline, which has been ongoing for the last few months. While the breakout attempt last Thursday initially failed, it has rebounded this week, which is a big positive in the short run, technically. The act of immediately pushing back to attempt to retest again after a failed breakout is thought to be a very good sign, so my thinking is that a move back over $275 should occur and help AAPL extend. While the earnings news seems to have been a success following Thursday’s market close, it’s important for the stock to break this $275 level to show real acceleration in a way that would help the market. Such a move, given its size within ^SPX1.06% and QQQ0.97% , has the potential to carry ^SPX1.06% over 7250, and this should happen into early May in my view. Overall, it looks right technically to be long AAPL0.63% ahead of its breakout.

Apple, Inc.

Equal-Weighted SPX (RSP1.43% ): Push to multi-day highs reflects the broadening — targets 205, en route to 208

The encouraging news from Thursday’s session revolved around seven sectors pushing higher than 1% in trading today, which helped the Equal-weighted S&P 500 ETF (RSP1.43% ) push to multi-day highs. This is precisely what the “Bulls” wanted to see, as it should help to carry the broader market back to new highs to join the cap-weighted ^SPX1.06% and QQQ0.97% in the days ahead.

Overall, I expect RSP1.43% to push up to test and exceed its prior highs at $205 en-route to 208 over the next 1-2 weeks.

Invesco S&P 500 Equal Weight ETF (RSP1.43% ) – Push to multi-day highs reflects broadening leadership; targets former highs near 205, en route to 208

Invesco S&P 500 Equal Weight ETF

Industrials (XLI2.68% ): Push back toward $178.80 prior highs likely as broadening accelerates; RSPN1.82% -$62.25 the equal-weight target

Today’s rally in Industrials to multi-day highs was similar to what also happened in quite a few other sectors, which had been languishing over the last two weeks.

REITS, Utilities, Energy, Communication Services, and Consumer Staples all made multi-day highs today, which adds to the near-term confidence about this rally having a chance to extend a bit more over the next week.

Industrial Select Sector SPDR ETF (XLI2.68% ) – Push back toward $178.80 likely as broadening leadership accelerates

State Street Industrials Select Sector SPDR ETF

Gold Stocks (GDX2.51% ): Steep short-term pullback now stabilizing near rising support — intermediate-term uptrend remains intact

Gold, Silver, and gold Stocks likely are nearing support and look attractive to buy from a risk/reward perspective for the following reasons:

- Gold’s short-term decline has not done any damage to its intermediate-term trends and Elliott-wave structure.

- The pullback in Gold Mining ETFs like VanEck (GDX2.51% ), shown below, has neared attractive trendline support.

- DeMark-related TD Buy Setups look to be in place on daily charts as of Thursday’s close. This suggests that the recent selloff in the precious metals should be nearly complete.

- I expect that FOMC independence might still be an ongoing concern, and incoming Chair Warsh’s job looks to be difficult given that the economy has heated up to the extent that traders are no longer pricing in cuts through next year.

Overall, GDX2.51% looks appealing, and I anticipate a bottoming out in Gold, Silver, and GDX2.51% , which could be starting this week.

Gains up to $104 look possible initially, and then over this level would allow for upside acceleration to test and exceed early-year highs for GDX2.51% .

Until long-term interest rates begin trending up dramatically, my expectation is that Gold, Silver, and the Mining stocks could still have a push higher back to all-time highs

VanEck Gold Miners ETF (GDX2.51% ) – Stabilizing near rising support after sharp pullback; intermediate-term uptrend remains intact

Vaneck Gold Miners ETF – GDX

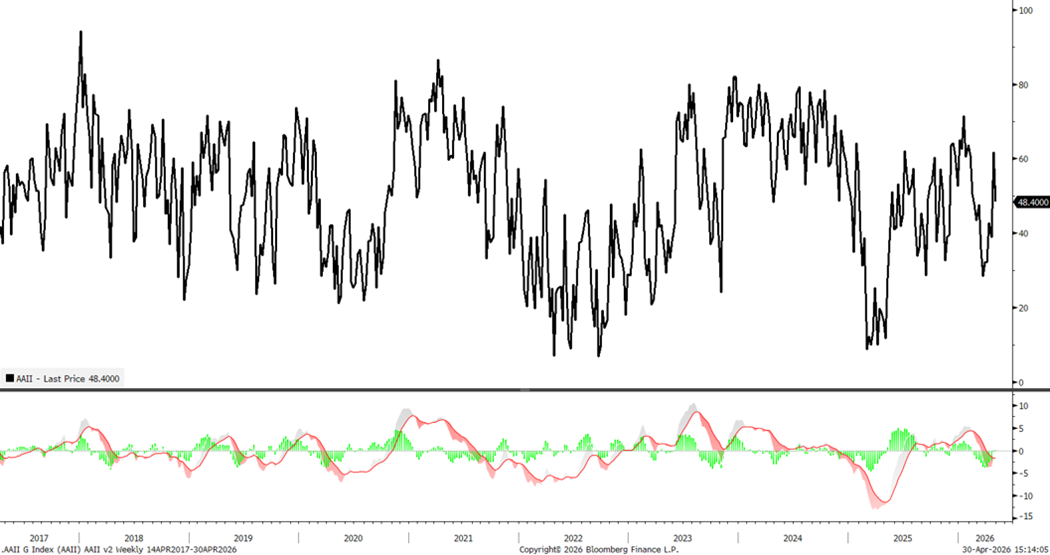

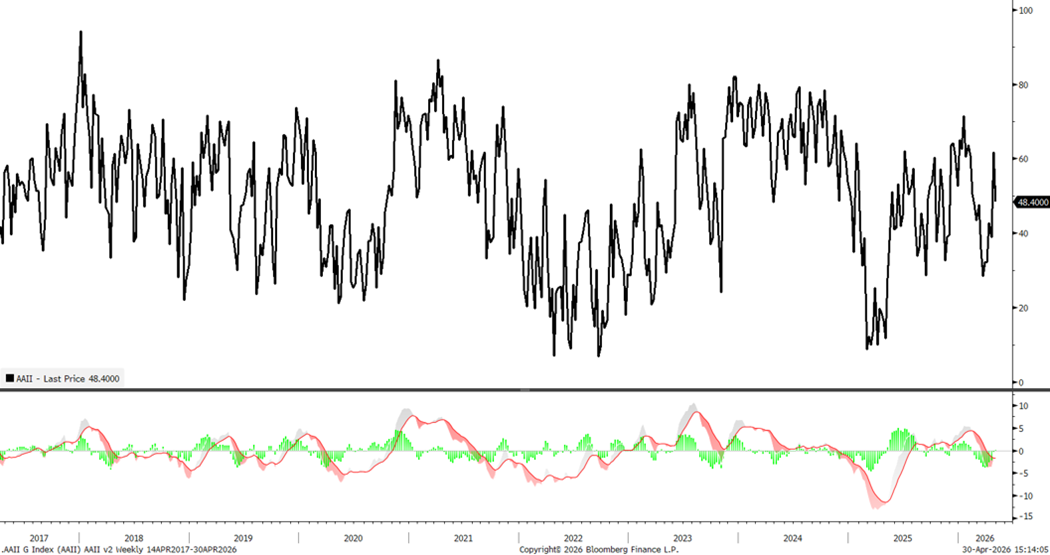

AAII Sentiment: Neutral elevated and Bull-Bear spread barely positive — a refreshing tell with no complacency to fade

Incredibly enough, despite the 12%+ rally in ^SPX1.06% since late March, AAII sentiment is largely neutral, with almost an equal number of Bulls to Bears.

This is interesting from a contrarian perspective and indicates that many remain in disbelief that the market can push higher, given that crude oil is still trending up while the Hormuz Strait remains closed.

My view is that this is a bullish “arrow in the quiver” for investors, and additional gains look likely based on earnings strength. This looks to overshadow the ongoing war and/or ramping up in geopolitical tension.

As this chart shows below, sentiment is largely neutral, not really bullish nor bearish. That’s a good sign for markets, as normally one might suspect that evidence of speculation and/or complacency was beginning to return to the market.

This looks premature as of now. The latest reading of nearly equal Percentage Bulls to Bears signals that there are investors not fully committed to the stock market rally. Normally, this signals that additional upside is certainly possible.

Bottom line, both technicals, along with strong earnings out of the many hyperscalers, are aligning right now to suggest gains, while sentiment is still rather muted.

AAII Investor Sentiment Survey – Bulls barely outpace Bears despite the rally; no complacency to fade

Bottom Line

Putting it all together, today’s broadening of leadership is the kind of confirmation I had been looking for, and gives me confidence that this rally has more gas in the tank rather than being on the verge of petering out. With ^SPX1.06% having cleared 7200 and a near-term target of 7250-7300, my view is that RSP1.43% , DJIA1.08% , and IWM2.24% should join ^SPX1.06% and QQQ0.97% at new all-time highs over the next 3-5 trading days, with all eyes on AAPL0.63% into earnings. AAPL getting over $275 in Friday’s trading session would be a bullish factor for this rally to continue next week, given AAPL0.63% ’s size. Furthermore, the AAII Sentiment poll’s continued elevated Neutral reading and barely-positive Bull-Bear spread tells me there is no complacency or speculative positioning to fade, and GDX2.51% ’s stabilization after a sharp pullback should be viewed as a buyable setup within an intermediate-term uptrend. Technically speaking, it’s right to lean bullish here, use any near-term weakness as an opportunity to add exposure, and look to Industrials retesting XLI2.68% -$178.80 and RSPN1.82% -$62.25 as further confirmation that this broadening leadership is here to stay. Stay tuned.

To unsubscribe from this email, please click here. You can also manage your email preferences and opt out of other types of emails by clicking here.